Special thanks to BDP for this write up. Take it away BDP!

So you’ve all heard of Fannie Mae and Freddie Mac… I’ve been doing some research at work on the topic so I thought I’d give a very high level overview.

A Brief History Of…

Fannie Mae (FNMA – Federal National Mortgage Association) was started by FDR as part of the new deal… it was a government, not a private corporation.

In 1968 LBJ privatized Fannie into a Government Supported Enterprise, aka GSE, due to “fiscal pressures.”

Now that Fannie was a private corporation, Freddie Mac (FHLMC – Federal Home Loan Mortgage Corporation) was started in 1970 to eliminate Fannie’s monopoly. Fannie and Freddie are almost identical corporations.

And They Exist Because?

Simple: to enable people to obtain the classic American Dream… their own home. Fannie and Freddie exist simply to make sure it’s easy for well qualified candidates to obtain mortgages at reasonable rates. They are mandated by Congress to do this. Â They’re definitely a good thing.

This government mandate gives them a few benefits a private lender will not have… simply, the implied faith of the US Government makes them an extremely safe investment. Not only that, they provide a guarantee of prompt and full payment on all of the securities they issue, which makes investors happy to take a lower interest on the securities they offer.

Oh, and since 1968 they are a private corporation so they have a responsibility to create wealth for their shareholders. Â More on this later.

So What Exactly Do They Do…Â

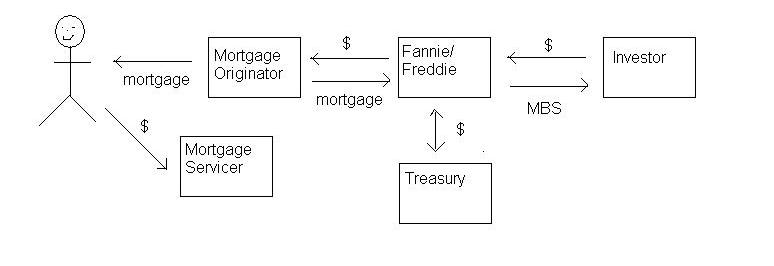

Check out this picture.

{kind=link}

So here you see a simplistic version of the process:

- Â Someone want’s a mortgage, they get it from a mortgage originator. If it’s a “conforming loan,” meaning it meets certain criteria, then we go on to step #2.

- The originator now sells the loan (in a bundle of many loans in most cases) on to FNMA for a small profit (usually in the half a percent range, plus fees).

- Fannie buys many loans from many originators, using low cost funds borrowed from the Treasury to do so.

- Fannie now pools these loans together into Mortgage-Backed Securities and sells them to investors. Fannie will also hold a portion of these loans and use them to issue its own shares to obtain more cheap funds and to turn a profit. Fannie’s securities are seen as extremely low risk, only slightly more risk than actual government debt, due to the implied backing of the US Government.

- Fannie pays back the Treasury.

- Loan Servicers collect money from the mortgages, pass them along to whomever earns those profits now… investors who hold the MBS’s that represent those loans, or to Fannie itself in the case of it’s own private portfolio. Fannie makes money because while your loan may be at 6%, they’re only paying 4% to the holder of their debt and they take a spread.

Which all means?

Loan originators are willing to issue you a mortgage because they know they can turn around and sell it at a profit to Fannie or Freddie. That means loans are plentiful and obtaining one isn’t too strenuous.

Fannie and Freddie stay afloat because they repackage and sell all of the loans they buy for a profit, or use them as collateral in loans where they also make a profit. Fannie and Freddie have a lot of liquidity thanks to the Treasury, so they continue to buy conforming loans.

All of this means you can get a conforming loan fairly cheaply and easily.

So That All Seems Good

Well, a few things are weird about Fannie and Freddie.

First of all, they’re not ACTUALLY guaranteed by the government… nobody has ever said they were. Â Secondly, they have two conflicting purposes… one to serve the public, one to make money for shareholders. The phrase I’ve heard is “Private Profit, Socialized Risk” meaning… profits go to speculators, but massive losses get paid by you and I the taxpayers.

Oh, and Fannie and Freddie aren’t regulated by the SEC, they only recently have been under regulation by the FHFA. And the lobbying arm of both was huge and well known for lavish fundraisers. Oh, also, Freddie and Fannie buy each others debt, so they’re intrinsically linked.

But nothing can go wrong with these, as long as folks pay their mortgages. Well…

Oops

So what happens when people stop paying mortgages in our little picture above? Well, Fannie stops receiving payments but has to continue to pay the holders of its MBS’s due to the guaratee it offers. After burning through a huge cash infusion from the Treasury, the stock did this.

{kind=link}

Ouch.

And this is definitely an oversimplification of what happened, but not a huge one.

So What Happened?

Secretary Paulson just bought you a big old stake in Fannie and Freddie. Something like an 80% stake. And if nothing further goes wrong it could earn the government money, but either way the government is now firmly in the game.

Morgan Stanley (hooray!) was asked to do an audit, something that the FHFA failed at, and came up with some stark conclusions:

In September the government basically seized both companies and put them into conservatorship. Secretary Paulson says:

“I attribute the need for today’s action primarily to the inherent conflict and flawed business model embedded in the GSE structure, and to the ongoing housing correction.”

In general this seems to be seen as the right move from both sides of the aisle, but it’s a huge and unprecedented move that will have ongoing affects for a long time to come.

However, this move basically eliminates the positions of every shareholder of the two companies… meaning investors are going to take enormous losses over this. Paulson has indicated he will work it out with the large and mid-sized investors, but nothing concrete has come out.

This was better summarized here:

“OK. Here is what is going on:

- Fannie Mae and Freddie Mac give the Treasury each 80% of their (common) stock and $1B (each).

- The Teasury promises to keep Fannie and Freddie solvent according to GAAP by lending it money at 10% per year.

- The Treasury promises to keep Fannie and Freddie liquid by buying its MBSs, financing the purchase by selling more Treasury bonds, and then holding the GSE MBSs to maturity.

- The Treasury, the Fed, and the FHFA will agree on an additional amount–a “commitment fee”–that Fannie Mae and Freddie Mac must pay to the Treasury starting in March of 2010.”

And what if we let them fail? From here:

“But let’s say that the Treasury did not support the debt of the mortgage agencies. The Chinese bought over $300 billion of that stuff and they were told that it is essentially riskless. The flow of capital from them and from other central banks, sovereign wealth funds, and plain old ordinary investors would shut down very quickly. The dollar would fall say 30-40 percent in a week, there would be payments system gridlock, margin calls at the clearinghouses would go unmet, and only a trading shutdown would stop the Dow from shedding half its value. Most of the U.S. banking system would be insolvent. Emergency Fed/Treasury action would recapitalize the FDIC but we would lose an independent central bank and setting the money supply would be a crapshoot. The rate of unemployment would climb into double digits and stay there. Many Americans would not have access to their savings. The future supply of foreign investment would be noticeably lower. The Federal government would lose its AAA rating and we would pay much more in borrowing costs. The deficit would skyrocket.”

Hopefully this very simple intro to the subject explained it enough for you, or sparks your interest to look more into it. It will affect every single US Citizen and many foreign nations as well, this is definitely worth knowing about.

I’ll take questions and respond in the comments

I like lettuce.

Good summary, but one thing that was neglected is that Sec. Paulson sacked the CEO’s of both Fannie and Freddie

“Herbert M. Allison former vice chairman of Merrill Lynch will take over for Fannie Mae, and David M Moffett, former vice chairman of US Bancorp, will take over for Freddie Mac.” (http://en.wikipedia.org/wiki/Freddie_Mac#Government_subsidies_and_bailout)

Yeah, two big hitters in the field running the companies will help establish a little more credibility for Fannie and Freddie (aka Frannie)

Awesome write up.

Great job!

Our economic stability is subject to the whims of the Chinese?

Thanks for the post. It explained a lot, and very well too.

Interestingly the US and China are in a bit of an economic cold war. Though the US holds the upper hand.

The US is a major consumer of products produced in China, so there is a steady supply of dollars flowing into the Chinese Economy. So, what are the Chinese to do with all of those dollars?

Option 1: Sell them, this would have serious impact on the quantity of products bought by the US. If China were to simply sell those dollars for yuan that impact would be 2 fold, since the glut of dollars for sale would drive down the value of dollar, additionally the increased demand for yuan would provide upward pressure on it’s value. So this would drastically effect the purchasing power of the US to buy Chinese goods (above and beyond how it would effect the US’s purchasing power for other foreign goods).

Option 2: Buy US Debt in the form of Mortgage Backed Securities or Treasury Bonds. This allows China to recycle the dollars back into the US economy without a direct influence on either currency’s value. Since this is the option the Chinese chose and they have such a large quantity of US debt they have put themselves in a bit of an untenable with the collapse of the US mortgage market. Since they again are in a situation where if they were to sell the assets they’ve acquired that would lead to an assured evaporation of value of those assets.

So, China cannot do anything too drastic with either it’s stockpile of US currency or it’s stockpile of US debt because it would entail a mutual annihilation of our economies.

Long Story Short: Diversify your portfolio.

I believe GZA said it best…

http://www.youtube.com/watch?v=poB8oSahSmM